Expensify

Expensify

Conviction 7.5/10

Portfolio Allocation if Buying: 1 ~ 3%

Intrinsic Value: $36 +/- 10%

Credit: Lu Jia Le for introducing this company

Business Overview

Expensify is a payments superapp that helps individuals and businesses around the world simplify the way they manage money.

App Features - Invoicing, Bill payments, Travel Booking, Reimbursements, Receipt scanning, etc.

They operate using a subscription-based, land and expand model, with monthly and annual subscriptions.

1. Management

Glassdoor Score: 9/10

The reason I didn’t give it a 10/10 is because of the low number of reviews.

Ownership Score: 9/10

CEO owns 13,695,820 shares , worth $616.3 mil @$45/share.

Holds 47.7% of voting power.

Gut Feeling of CEO 7.5/10

Exhibits “Conscious Capitalism” mindset

Understands the importance of building a culture

Wears T-shirt & Jeans

No bullshit, straight to the point, get shit done attitude.

Serves a higher purpose

Easy to understand S-1

Very clear on what the company does what he wants to accomplish through Expensify

Product / Services

Ranked best for SMBs on a highly reliable site.

Among the top searches on google - “best expense report software”

Ranked #4 on G2.com

Ranked 1st Page on TrustRadius & softwareadvice.com.sg

Financials

Revenue

2019: $80 mil

2020: $88 mil

1st Half 2020: $40.6mil

1st Half 2021: $65 mil

Grew only 10% from thru pandemic, 2019 - 2020. (Not recession proof)

Reaccelerated to 61% growth for 1H 2021. (Good)

Gross Profit Margin (%)

2019: 60%

2020: 63%

1H 2020: 62%

1H 2021: 76%

62% —> 76% in 1H 2021 . Exhibited amazing operational leverage!

We usually don’t see that big of a jump in GPM.

Operating Income

2019: $1.2 mil

2020: $5.6 mil

1H 2020: $6.3 mil

1H 2021: $19 mil

Already operating income positive and trending up!

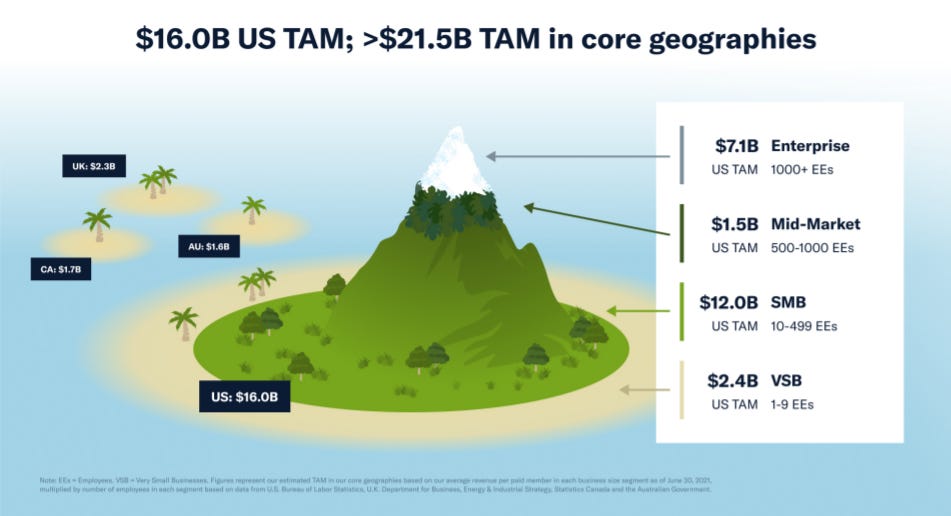

Market Opportunity

Large but competitive - Intuit, Oracle Corporation (NetSuite), SAP AG (Concur) and Workday. Plus many more on comparison websites like G2.com , TrustRadius.

Given their 2021E revenue of $140 mil and expecting them to take 30% market share, their growth runway is about 267x.

What makes Expensify stand out?

As a non-user, we can get a feel of much customers love the platform by looking at abstract data.

One way is to look at their Net Seat Retention (NSR) as provided very clearly & conveniently in their S-1 (bonus points).

NSR 2019 : 119% (Good)

NSR 2020 : 98% (forgivable due to pandemic)

On top of the pandemic, Expensify mainly serves SMB(s) which makes their low NSR even more forgivable as SMB(s) in general are more heavily affected than large companies.

Customers ceased (or paused) operations, and scaled back usage of Expensify platform as their business travel and other expenses declined.

Stellar reviews from comparison websites and especially ranking 1st for

“Best Expense Management Software for SMB(s)”.

Strategic - Dominating the SMB market is strategic because SMB(s) are the cornerstone of the global economy, making up over 99% of businesses and approximately 70% of employment in Organization for Economic Cooperation and Development ("OECD") countries.

Out of these population, many will move on to Larger corporations and since a large number of the workforce is already familiar with Expensify, they are incentivized to adopt the most commonly used platform.

Think of how adobe targeted schools and offering them software at low-cost. By the time students graduate, the industry are forced to adopt adobe as to avoid re-training their employees on another software.

Conclusion

Lots to like about this company, ticks a lot of boxes except for it being heavily affected by the pandemic.

There are definitely better companies out there hence the small portfolio allocation. Nevertheless, still a decent company at a fair price.