Flywire

Description

Flywire’s mission is to deliver the most important and complex payments.

They operate in 4 main industries which are lagging behind in payment solutions namely - Education, Healthcare, Travel, and B2B.

Numbers:

Served 2250 clients across 240 countries.

Transacted $7.5B in payment volumes in 130 supported currencies.

Dollar Based Net Retention Rate - 118%

Client Retention - 97%

Net Promoter Score (NPS) - 64

Market Opportunity

Flywire estimates the annual payment volume from their 4 core markets to be $1.7T.

Assuming that to be true, Flywire has only tapped 0.7% of its market opportunity.

Management Team

Michael Massaro, CEO

20 years of background in global payments, mobile software and hardware, and e-billing at high growth technology companies, including edocs, Inc. (later acquired by Siebel Systems) and Carrier IQ.

Rob Orgel, COO

20 years in the technology/payments ecosystem.

Prior to Flywire, Mr. Orgel served in various roles at Apple Inc. from 2010 to 2019 where he was part of the leadership team that developed, launched, and grew the Apple Pay as well as Apple Card. Prior to his time at Apple Inc.

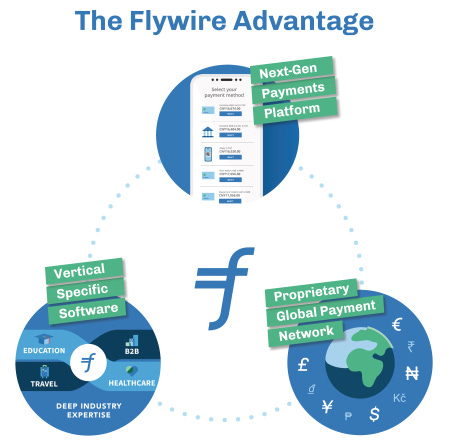

Differentiation Points

Next-Gen Payments Platform

Solution Suite -

Tailored invoicing

Settlement and reconciliation tools

Single sign-on and checkout

Recurring payments

Split payouts (Eg. For a $100 transaction, customers can use debit card to pay $50, and credit card to pay remaining $50)

In addition, Flywire leverages deep data and analytics to help clients understand their customers’ historic payment behavior to determine if the customer is eligible to pay by installments.

Proprietary Global Payment Network

Accepts non-conventional payment methods including Alipay, Boleto, PayPal/Venmo, and Trustly.

Customers can use any currency of their choice.

Cost Savings:

Flywire can save up to 3% in fees.

Having moved over $16 billion, Flywire has tremendous negotiating power with their payment processing partners. This allows them to reduce costs, and pass savings along to their clients.

How to reduce costs when accepting travel payments <—- Link for more detailed explanation on how Flywire helps save on fees.

Flywire can help reduce the merchant fees on credit card transactions to around 1.5%, and the cardholder fees to around 2%, giving an all-in cost of around 3.5%

Vertical Specific Software

Each client receives tailored solutions from Flywire’s team who has deep industry expertise, providing a better customer experience and eliminating time-consuming customer calls to make their operations more efficient.

Competition

The top direct competitor is Western Union (WU). I do not see WU as a threat and see Flywire continue to snatch market share based on their superior solution and stronger client reviews.

Flywire vs Western Union <— Check this link for comparison scores.

Flywire’s primary competition consists of

local, regional and global banks

Remittance companies

Integrated payment providers focused on cross-border payments

B2B payments platforms

Vertical-specific software solutions offered by local niche players

Many legacy payment providers are hindered by limitations such as antiquated technology systems, insufficient solution and service offerings, poor user experiences, and unsatisfactory client and customer support. Flywire’s modern technology stack, combined with their innovative and flexible suite of solutions, addresses many of the issues that clients face today, including:

• friction in client and customer experiences;

• lack of a scaled global network;

• limited software and payments offerings;

• inability to adapt to new technology; and

• unsophisticated fraud prevention and risk management tools.

Flywire believes to compete favorably on the basis of these factors.

For solutions such as Stripe or Authorize.net, there are multiple fees involved when processing an international customer’s credit card. The first is the merchant/receiver fee, which is typically a percentage, plus a fixed fee (e.g. 2.9% + .30 per transaction). If currency conversion is required, additional fees (typically around 1%) often apply.

Valuation

Year: 2019 2020

Revenue: $95mil $134mil

Gross profit: $58.2mil $84mil

Gross margin: 61.3% 63.7%

Revenue increased 41% YoY through unforgiving circumstances.

Gross margins expanded ~2%, showing operating leverage at scale.

Running a DCF calculation with the following parameters assumed

30% CAGR (Year 1 to 5) , 15% CAGR (Year 6 to 10), 10% CAGR (Year 11 to 20)

25% Operating Cash Flow Margin in future

We arrived at an intrinsic value of $22.30

Personally, I am willing to wait for the price to drop to as low as $21 because I have low to medium conviction in Flywire.

Risks

Let’s imagine that our investment in Flywire underperformed the S&P500, delivering flat returns. What could be a reason for that?

Strong competition from larger players, offering better / cheaper solutions.

Cryptocurrency becomes the De Facto mode of payment.

So far, these are 2 things I could think of. If you have a stronger bear case, please feel free to leave a comment!